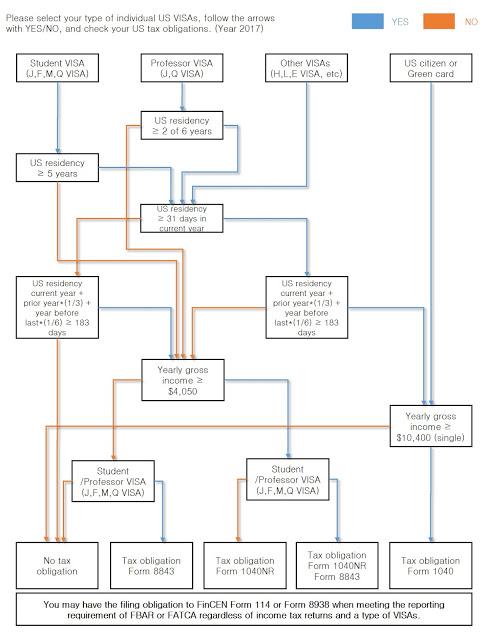

Test for US tax obligation to an

individual on VISAs

☞ The following statement is about test for US tax

obligation to an individual on VISAs, and is not legally binding.

The US tax obligation to an individual may differ depending on the individual VISA, residency, and Incomes. And the individual, which possesses foreign bank accounts, may be subject to the report of foreign financial asset account (FBAR and FATCA) regardless of a type of VISAs.

Please click the following picture to

enlagre

IRS

Taxation of Aliens by VISA Type and Immigration Status

|

Aliens on A-1; A-2; A-3

Visas—Employees of Foreign Governments

|

A-1

|

A-2

|

A-3

|

|

|

|

Aliens on B-1; B-2 Visas—Visitors

for Business / Visitors for Pleasure

|

B-1

|

B-2

|

|

|

|

|

Aliens on C-1; C-2; C-3

Visas—Aliens in Transit Through the USA

|

C-1

|

C-2

|

C-3

|

|

|

|

Aliens on D-1; D-2 Visas—Alien

Crew Members of Ships and Aircraft

|

D-1

|

D-2

|

|

|

|

|

Aliens on E-1; E-2; E-3

Visas—Treaty Traders and Treaty Investors

|

E-1

|

E-2

|

E-3

|

|

|

|

Aliens on F-1; F-2; F-3

Visas—Academic Students

|

F-1

|

F-2

|

F-3

|

|

|

|

Aliens on G-1; G-2; G-3; G-4; G-5

Visas—Employees of International Organizations

|

G-1

|

G-2

|

G-3

|

G-4

|

G-5

|

|

Aliens on H-1; H-2; H-3; H-4

Visas—Workers in Specialty Occupations

|

H-1

|

H-1b

|

H-2

|

H-3

|

H-4

|

|

Aliens on I-1 Visas—Members of

the Foreign Press

|

I-1

|

|

|

|

|

|

Aliens on J-1; J-2 Visas—Exchange

Visitors

|

J-1

|

J-2

|

|

|

|

|

Aliens on K-1; K-2; K-3; K-4

Visas—Fiance or Spouse of U.S. Citizen

|

K-1

|

K-2

|

K-3

|

K-4

|

|

|

Aliens on L-1; L-2

Visas—Intracompany Transferees

|

L-1

|

L-2

|

|

|

|

|

Aliens on M-1; M-2; M-3

Visas—Vocational Students

|

M-1

|

M-2

|

M-3

|

|

|

|

Aliens on N-8; N-9 Visas—Parent

/Child of Lawful Permanent Resident

|

N-8

|

N-9

|

|

|

|

|

Aliens on O-1; O-2; O-3

Visas—Aliens with Extraordinary Ability

|

O-1

|

O-2

|

O-3

|

|

|

|

Aliens on P-1; P-2; P-3; P-4

Visas—Alien Athletes and Entertainers

|

P-1

|

P-2

|

P-3

|

P-4

|

|

|

Aliens on Q-1; Q-2; Q-3

Visas—Cultural Exchange Visitors

|

Q-1

|

Q-2

|

Q-3

|

|

|

|

Aliens on R-1; R-2

Visas—Religious Workers

|

R-1

|

R-2

|

|

|

|

|

Aliens on S-5; S-6; S-7

Visas—Aliens Supplying Critical Information On Criminal Activity

|

S-5

|

S-6

|

S-7

|

|

|

|

Aliens on T-1; T-2; T-3; T-4; T-5

Visas—Victims of Trafficking in Persons

|

T-1

|

T-2

|

T-3

|

T-4

|

T-5

|

|

Aliens on U-1; U-2; U-3; U-4; U-5

Visas—Victims of Criminal Activity

|

U-1

|

U-2

|

U-3

|

U-4

|

U-5

|

|

Aliens on V-1; V-2; V-3

Visas—Spouse / Child / Parent of Lawful Permanent Resident

|

V-1

|

V-2

|

V-3

|

|

|

|

Aliens on TN; TC; TD

Visas—Professional Business Person From Canada or Mexico

|

TN

|

TC

|

TD

|

|

|

|

|

|

|

|

|

|

|

Aliens on the Visa Waiver Program

|

|||||

|

Alien Visitors From CFA

Countries—Micronesia / Marshall Islands / Palau

|

Micronesia

|

Marshall Islands

|

Palau

|

||

|

Asylees—Aliens Who Have Been

Granted Asylum in the USA

|

|||||

|

Refugees—Aliens Who Entered the

USA as Refugees

|

|||||

|

Parolees—Aliens Allowed to Enter

the USA Temporarily

|

|||||

|

Aliens in TPS—Temporary Protected

Status

|

|||||

|

Lawful Permanent Residents—Green

Card Holders

|

|||||

Source:

IRS

[미국세무] 2017년와 2018년도 귀속 미국 개인 납세자를 위한 세무회계 정보

미국 비자별 미국세무신고의무 테스트

☞ 다음은 미국 비자별 미국세무신고의무 자진 테스트이며 법적인 효력은 없습니다.

개인이 보유하고 있는 미국 비자와 거주상태, 소득에 따라 미국세무신고의무가 다를 수 있습니다. 또한 해외금융자산계좌를 보유하고 있는 해당 개인은 비자 종류와는 상관없이 해외금융자산계좌 신고 (FBAR및 FATCA)의 대상이 될 수 있습니다.

아래 그림을 클릭하면 크게 볼 수 있습니다.

IRS Taxation of Aliens by VISA Type and Immigration Status

출처: IRS

댓글 없음:

댓글 쓰기